Stories and lessons from an unexpected journey in finance.

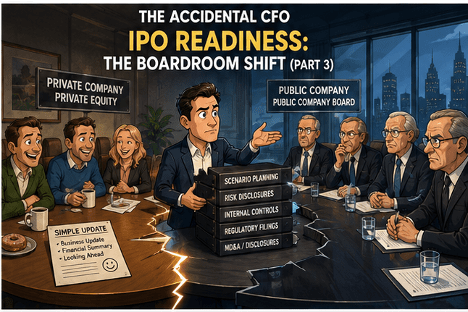

The informal, conversational reporting cadence that works perfectly in a PE-backed environment absolutely does not translate to the public markets. The governance expectations of a public company board are structurally different, and the CFO who does not adapt their communication model before the IPO will spend their first year of public company life desperately trying to catch up. The key differences in this transition are not merely cosmetic; they are highly substantive and require a complete operational shift.

Public company boards expect rigid, highly formalized monthly financial reporting at an absolute minimum, alongside quarterly deep dives aligned directly to the earnings cycle. They also expect regular one-on-one director engagement between official meetings. More importantly, they expect proactive, highly specific risk disclosures packed with concrete scenario analysis and active mitigation plans, rather than general risk acknowledgment. The CFO who simply presents upside scenarios without providing detailed, quantified risk analysis loses their credibility incredibly quickly.

You must also proactively establish a direct, active relationship with the audit committee. The audit committee of a public company board holds a direct relationship with the external auditors and carries a formal oversight responsibility for the financial close and controls environment. This relationship must be managed actively, not reactively, ensuring they are fully briefed on all infrastructure remediation efforts well ahead of any filings.

Finally, the CFO owns the critical alignment between what the board hears and what the open market hears. Any forward guidance provided to external investors must be strictly consistent with, and ideally derived directly from, the financial framework the board has officially approved. You need to cement this public company board reporting model at least two to three quarters before the IPO officially closes. Your very first public board meeting should never be a learning experience. An IPO-ready CFO fundamentally understands that keeping the board informed is no longer enough. The board must be operating fully to the new public company governance model before the S-1 is even filed. Waiting until the ringing of the bell to shift these critical communications will leave you exposed and vulnerable during your most critical months of trading.

Transitioning a board’s governance style is rarely an easy task. What is the biggest friction point you have seen when upgrading board reporting from private to public standards?

#TheAccidentalCFO #INERSEC #CorporateGovernance #BoardOfDirectors #IPO

Leave a comment